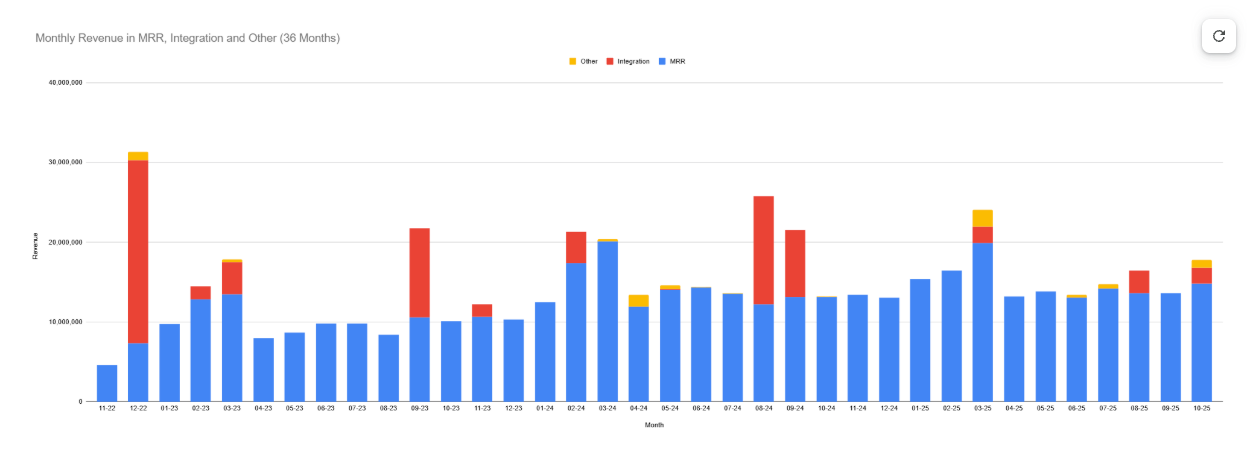

Revenue: The 36-month revenue trend shows steady expansion in our recurring revenue base. MRR has grown from ~$33,000 per month in late 2022 to consistently $85,000–$110,000 per month in 2025, representing a ~3x increase in recurring revenue. This translates to ARR growth from approximately $470,000 to over $1.3 million, marking a meaningful strengthening of our predictable revenue engine. Integration and Other revenue streams continue to create episodic upside, confirming our ability to monetize enterprise implementations when strategically aligned.

At the same time, the chart highlights our central challenge: while we are growing, the pace remains gradual. For 2026, a key agenda will be accelerating MRR growth.

Operating Profit: The 36-month operating trend shows a disciplined and measurable progression toward profitability when viewed in USD terms. In the early period, monthly operating losses ranged from approximately $200,000 to $300,000, reflecting the heavy investments required to build the core product, scale infrastructure, and establish early market presence. Beginning mid-2023, losses steadily narrowed as we improved operational efficiency, optimized headcount allocation, and strengthened our recurring revenue base. By late 2024 and throughout 2025, the slope of improvement becomes even clearer, with losses consistently shrinking to the $50,000–$120,000 range and several months approaching near breakeven.

In the most recent periods, we begin to see slightly positive operating profit, demonstrating that our financial model is now structurally sound. With fixed costs largely stabilized and incremental revenue carrying higher contribution margins, we are entering a phase where growth increasingly translates directly into operating leverage. As we accelerate MRR expansion in 2026, we expect sustained profitability and progressively stronger free cash flow.

Gross Margin: The gross margin profile over the past 36 months demonstrates strong unit economics and meaningful improvement in operational efficiency. Margins consistently range between 70% and 90%, with several periods approaching mid-90%, underscoring the scalability of our software-driven cost structure. Early fluctuations were primarily tied to one-time infrastructure expenses and onboarding costs associated with enterprise deployments. As our platform matured, automation increased, and service delivery stabilized, margins trended upward—settling into the 80–90% band throughout 2024 and 2025. The most recent months show our highest margins to date, signaling optimized cloud utilization, lower variable cost per scan, and improved pricing discipline. These margins place us firmly within top-tier SaaS benchmarks and provide substantial leverage as we scale MRR. With continued infrastructure tuning and higher volume throughput, we expect gross margins to remain robust and potentially expand further as we enter 2026.

The annualized revenue-per-headcount trend underscores a dramatic improvement in organizational efficiency and operating leverage. In the early period, annualized productivity ranged from $12,000 to $36,000 per employee, reflecting the natural imbalance between team size and revenue during initial product development. As the platform matured and commercial execution strengthened, productivity rose into the $36,000–$72,000 range through 2023–2024. In 2025, the company achieved a major step-change: several months now operate at an annualized $132,000–$156,000 per employee, placing us in the top quartile of lean SaaS organizations globally. This 4–5× improvement over the last three years demonstrates disciplined headcount management, stronger monetization, and a business model that now scales with significantly greater efficiency. As we deepen recurring revenue in 2026, we expect revenue-per-head to remain a core competitive strength and a key driver of sustained profitability.

Our customer base consists of the top players across Japan’s most influential industries, demonstrating both the breadth and credibility of our platform. We serve leading brands in retail, apparel, fitness, insurance, sports, manufacturing, and national institutions as well as government-backed organizations. This diversified portfolio confirms that our technology is trusted by category leaders who demand reliability, scale, and precision. It also reinforces a key strategic advantage: our platform is industry-agnostic, enabling us to operate as the body intelligence layer powering innovation across multiple high-value sectors.